On the heels of my return from Phoenix Biosciences Core and a talk about the Arizona startup ecosystem, Texas announces ARPA-H funding, Advanced Research Projects Agency for Health supporting transformative biomedical and health breakthroughs. It didn’t luck into it with a last-minute pitch deck and a prayer. Four major cities put aside their egos, formed a coalition, and outmaneuvered the coasts at a game the coasts invented.

Thomas Graham, founder of Crosswind Media & Public Relations and the strategist behind the Coalition for Health Advancement and Research in Texas (CHART), wrote in the Dallas Morning News that Texas “licked partisan politics and regional rivalries” to land one of the most coveted bioscience investments in the country. He described a tone of collaboration across Houston, Dallas, Austin, and San Antonio, noting, “We compete, but we also collaborate.” Graham framed the dynamic between Texas cities as something close to “co-opetition,” a balance of healthy competition paired with intentional collaboration to win against other states, not each other. I say, “finally,” with a sigh of relief about Texas. He’s right; that spirit is rare and it matters enormously. When the Dallas Regional Chamber’s Kelly Cloud was asked to highlight recent developments in the Dallas economic development landscape, she paused and responded: “How much time do I have?” Let’s look at why.

Because Graham’s article, and the institutional wins he rightly celebrates, tells a story to which I want to add. Where I focus, is among the questions that should follow every announcement of a new hub, a new $6.5 billion Eli Lilly investment, or a new CPRIT allocation: what does it mean for the startups, the venture capitalists, and the entrepreneurs? Not the research. Not the recruitment of established pharmaceutical firms and not the real estate, but for our slice of an economy where risk is highest. The people who are building the companies that will either commercialize the science emerging from these institutions or watch that science get licensed, shelved, or exported to Boston.

That question, is the one few answer honestly because the answer is complicated, uneven, and in some cases, embarrassing relative to the scale of the institutional assets. So, let’s answer it.

Article Highlights

- The Institutional Foundation Is Formidable (and That’s the Easy)

- Where the Startups Actually Are

- The Venture Capital Landscape: Promising but Incomplete

- Startup Development Organizations: The Good, the Missing, and the Siloed

- The 10 Considerations Applied to Texas Biosciences

- The Policy Gap That Nobody Wants to Talk About

- Next for Texas Biosciences

The Institutional Foundation Is Formidable (and That’s the Easy)

Texas’ bioscience infrastructure would make most countries jealous, let alone most states. CPRIT (the Cancer Prevention and Research Institute of Texas) is a $6 billion initiative, making Texas the largest state funder of cancer research in the nation and the second-largest public funder behind only the National Cancer Institute. As of August 2025, CPRIT has awarded more than $3.9 billion through over 2,148 merit-based grants across 149 Texas institutions, organizations, and companies. One county alone has received $2.3 billion of that, roughly 60 percent of the total. CPRIT allocates approximately $70 million annually specifically for company investments through milestone-based contracts, covering SEED, therapeutics, diagnostics, and new technology company awards. That is non-dilutive capital (meaning founders don’t give up equity for it), and it flows through a legitimate peer-review process that should be the envy of every state in the country.

The Texas Medical Center in Houston is the largest medical complex on the planet. UT Southwestern, in Dallas, is a research powerhouse that attracts federal funding at scale. Dell Medical School at UT Austin only opened in 2016 and has already begun reshaping the capital city’s life sciences trajectory. San Antonio generates more than $44 billion annually through its bioscience and healthcare sectors and houses the Texas Biomedical Research Institute alongside a substantial military medical community through Brooke Army Medical Center. The ARPA-H Customer Experience hub at Pegasus Park in Dallas sits within a $2.5 billion national health innovation network. UT San Antonio’s Barshop Institute just secured up to $38 million from ARPA-H for the first nationwide clinical study in healthy longevity. The proposed Dementia Prevention and Research Institute of Texas (DPRIT), modeled after CPRIT, would add another $3 billion if approved.

But ingredients don’t cook themselves and as I’ve looked to other hubs of innovation in health, we want to look to the strengths and weaknesses of what we can cook. A state that accumulates this much institutional firepower while leaving the startup pipeline structurally incomplete is a state building a mansion on a dirt road.

Where the Startups Actually Are

The 2025 Austin Bio & Health Report, authored by Jason Scharf and Jani Tuomi, documented that Austin alone is home to over 1,100 bio and health companies, employing 21,000 people, and generating a total ecosystem valuation of $77 billion, a staggering 45 percent surge in 2025 alone that pushed total value growth to a 52 percent compound annual growth rate over the last eight years. Venture capital investment has reached $1.6 billion in bio and health sectors in 2025 alone, vaulting Austin to 6th nationally in health sector VC funding, up from 18th in less than a decade, with only roughly $100 million separating Austin from overtaking legacy hubs Los Angeles and San Diego. Bio and health now capture one in five venture dollars invested in Austin, up from just 12 percent. The report identifies multiple companies that have crossed $100 million in valuation alongside several unicorns valued above $1 billion, with 665 additional startups below the $100 million threshold forming the base of the pipeline. The top five investment deals of 2025 tell the story: Function Health at $298 million Series B, Curative at $150 million Series B, Harbor Health at $140 million, Ollin Biosciences at $100 million Series A, and Alleviant Medical at $90 million.

But they also conceal a pattern that anyone who has studied startup ecosystem capacity building will recognize. Most of that value is concentrated at the top; the middle is thin and the bottom, the aspiring founders, the first-time biotech entrepreneurs, the researchers who have commercializable science but no idea how to form a company, that population is largely underserved.

Dallas healthcare startups raised $448 million in 2025, with notable companies including Osteal Therapeutics, MicroTransponder, ReCode Therapeutics, and Colossal Biosciences (which recently became Texas’ first decacorn at over $10 billion in valuation). Houston closed out 2025 with significant biotech funding rounds alongside its energy-tech corridor. The Texas Medical Center Innovation’s 2025 Accelerator for Cancer Therapeutics supports over 50 startups advancing immunotherapy, diagnostics, and targeted cancer drugs.

The 2025 Report frames these cities as the “Texas Bio Triangle,” one interconnected mega-region powered by four distinct hubs. The VC funding breakdown across the triangle tells an important story: Austin led with $1.6 billion, Dallas-Fort Worth contributed $218 million, San Antonio $151 million, and Houston $108 million, for a combined total of $2.07 billion in health sector venture capital across the state. Austin is positioned as the tech-enabled innovation and commercialization hub; Houston as the home of foundational discovery and clinical trials at the Texas Medical Center; San Antonio as the center of applied research and military medicine; and Dallas-Fort Worth as the scale, distribution, and financial gravity of what is being called “Y’all Street.”

Jason Scharf, the early-stage bio and health investor who co-authored that report and hosts the Austin Next podcast, has been one of the most consistent voices making this exact point. Scharf, who previously held leadership roles in strategy and market intelligence at Illumina, BD, and Amgen, would likely tell you something that echoes what he’s said publicly, “An ecosystem isn’t built when a giant established player moves in. It grows and thrives by helping the companies already here go from scrappy beginnings to real winners, even unicorns. That is how Austin’s Bio & Health stack went from a small outpost to a hub of real significance.” He’s been hammering the thesis that Austin’s path isn’t to recruit big pharma but to grow its own, and he’s correct. The lesson from Boston and the Bay Area wasn’t that big companies moved there; it was that startups grew there, and the big companies followed.

Anna Sizova, an Austin-based physician, pediatric endocrinologist, and HealthTech innovation leader who connects founders, investors, clinicians, and global partners across 40+ countries through her community IMPACT-HEALTHTECH, frames the challenge plainly: “Texas has the institutions, the patients, and the science. What it’s still building is the translation layer; people who understand both clinical development timelines and startup velocity. Founders need someone who can help them navigate FDA pathways, de-risk their regulatory strategy early, and avoid spending their runway on mistakes the pharma and CRO world solved decades ago. That gap between a university breakthrough and a fundable company with a real development plan is where most of this potential quietly disappears.”

For Sizova, this isn’t abstract. As a physician who has spent over two decades at the intersection of clinical research, global health, and the startup ecosystem, she has watched brilliant science stall not for lack of funding, but for lack of translation; the kind that only comes from someone who has stood inside a clinical trial and inside a pitch room. Her work building IMPACT-HEALTHTECH, co-founding an AI surgical startup, and mentoring founders through programs like Nucleate has made that gap clear: the distance between a published paper and a funded company with a credible IND pathway is vast, and most ecosystems have almost nothing filling that space.

The Venture Capital Landscape: Promising but Incomplete

Texas’ venture capital ecosystem for biosciences is real, growing, and rapidly maturing, though still not fully proportional to the institutional assets it appropriately should be capitalizing. S3 Ventures, the largest and longest-serving VC firm born in Texas, manages over $1 billion in assets across healthcare technology and B2B software and just closed a $250 million Fund VIII. Silverton Partners brings over $700 million under management. ATX Venture Partners, PTV Healthcare Capital, and LiveOak Venture Partners all play active roles in early-stage health and biotech.

The 2025 Report reveals substantial new venture capital dry powder entering the Austin bio and health market: 8VC closed a $998 million Fund VI, Sante Ventures raised a $330 million Fund V, and Virtue VC launched a $56 million Fund II. The report identifies 13 venture capital firms with bio and health as their sole investment focus in Austin (including 4D Capital, Create Health Ventures, HealthQuest Capital, KdT Ventures, Sante Ventures, TEXO Ventures, and Virtue VC), eight additional firms with bio and health as a key focus (including 8VC, Next Coast Ventures, and S3 Ventures), and 19 more that have made bio and health investments.

That capital stack is diversifying and deepening in ways that were simply not true two years ago.

Bios Partners, a venture capital firm explicitly focused on identifying advanced biotech in overlooked and under-invested U.S. markets, directly addresses what they call “geographic favoritism” in venture capital, the well-documented tendency of capital to concentrate on the coasts. Their thesis is that great science is evenly distributed throughout the country, but venture funding is not. They’re right.

National firms have significantly increased their Texas activity: Sequoia Capital, Andreessen Horowitz, and Kleiner Perkins have all made Dallas investments in 2024 and 2025. The influx of national capital has helped Texas startups scale more quickly, but it has also driven up valuations and created a dynamic where the very best deals flow upward to coastal capital while the middle tier of promising-but-not-yet-flashy startups struggles to find appropriate funding locally.

This is exactly the pattern I’ve written about extensively. Venture capital avoids your startup ecosystem not because investors are ignorant of what’s going on but because the ecosystem hasn’t built the density of deal flow, the mentor infrastructure, and the market-readiness preparation that makes investing rational. When I talk about why startup ecosystems fail because of investors, I’m not blaming VCs for being cautious, I’m blaming the ecosystem infrastructure for not making caution unnecessary. You can’t yell at money for being rational, you have to make your region so structurally sound that money has no excuse not to show up.

Startup Development Organizations: The Good, the Missing, and the Siloed

The organizational infrastructure supporting bioscience startups in Texas is a mixed bag. Some of it is excellent but much of it is fragmented. And a disturbing amount of it is doing the same thing three other organizations are already doing, in isolation, while using the word “collaborative.”

BioAustinCTX serves as the Central Texas life science industry organization, working to bring together entrepreneurs, infrastructure, capital, and talent. The ACC Bioscience Incubator provides wet lab space and connections. The Texas Medical Center Innovation operates accelerators in Houston. The Biotechnology and Healthcare Industry Alliance of North Texas (BHIANT) focuses on workforce development and industry partnerships.

A significant infrastructure development that the 2025 Report highlights is The Domain, in Austin, emerging as the bio and health district. The University of Texas has opened 10,000 square feet of Innovation wet labs there, and the $2.5 billion UT Medical and MD Anderson campus has pivoted from its originally planned downtown location to The Domain, with new zoning unlocking future development. This is precisely the kind of purpose-built, density-creating infrastructure that bioscience startups need; not another coworking space with a microscope on the shelf, but actual wet lab facilities near research talent with room to grow.

But here’s the problem, and it maps precisely to Consideration #1 the 10 Considerations of why startup ecosystems fail: silos destroy throughput. Universities run their commercialization programs, Chambers run theirs, Incubators build cohorts in isolation, and Government agencies maintain parallel databases. Everyone “supports entrepreneurship,” yet founders navigate a maze where every door leads to a different map. In the biosciences, this fragmentation is even more damaging because the cost of entry is higher, the timelines are longer, and the regulatory complexity means that a founder getting the wrong advice at the wrong time doesn’t just waste six months; they can waste years and millions of dollars pursuing a regulatory strategy that was never viable.

The 10 Considerations Applied to Texas Biosciences

Let me walk through the 10 Considerations framework as it applies specifically to the Texas bioscience startup economy, because this is the operating manual for what Texas needs to address if it wants the startup layer to match the institutional layer that Graham and others rightly celebrate.

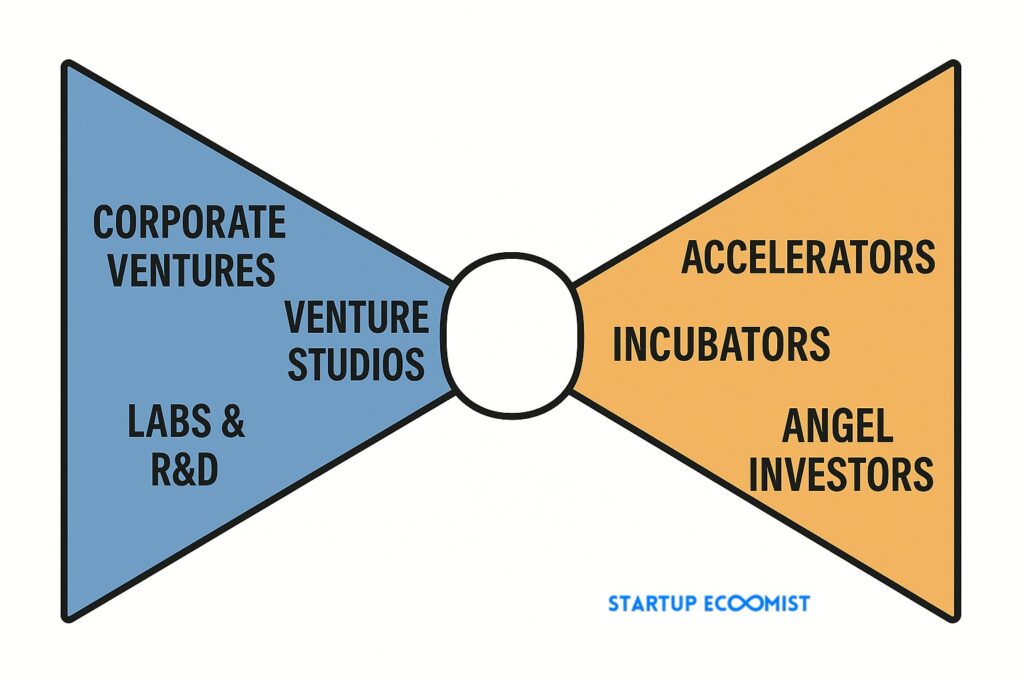

1. Overcoming Silos. Texas biosciences suffers from the same fragmentation problem every ecosystem does, except the stakes are higher. CPRIT operates in one lane, BioAustinCTX operates in another, and TMC Innovation runs its accelerators without enough structural connection to what Austin or Dallas are doing for early-stage founders. The ARPA-H hub in Dallas should, theoretically, create connective tissue across all four cities, but that depends entirely on whether anyone architects that connection deliberately. Graham’s “co-opetition” framing is wonderful; it needs to become operational through shared CRMs, unified mentorship standards, and consistent deal-flow pipelines that move founders to the right resources regardless of which city they started in.

2. The Missing Middle. This is Texas biosciences’ biggest vulnerability. The state has excellent resources for nascent researchers (CPRIT grants, university tech transfer offices, incubator space) and excellent resources for established companies (ARPA-H partnerships, TMC infrastructure, state incentive programs). Between those poles sits a canyon. The high-growth, pre-scale biotech startup that has initial data but needs mentorship, capital-readiness preparation, B2B customer access, and regulatory strategy support; that company dies in the gap more often than it survives it. The missing middle is where Series A funding should live, where fractional CSOs and regulatory affairs executives should be available, and where applied R&D partnerships with pharma companies should be actively brokered. Most of that doesn’t exist at scale in Texas; it needs to.

3. Funding the Actors. Every bioscience ecosystem in Texas relies on a handful of people who are doing the connecting, mentoring, and advising work that makes the system function: Most are underfunded. Many burn out. Cities pour millions into ARPA-H bids and corporate recruitment incentives while asking the people who actually run the startup programs to survive on sponsorship revenue and ticket sales. Stable, multi-year operational funding for ecosystem builders is not a nice-to-have, it’s infrastructure. Treat THEM like infrastructure or watch the infrastructure collapse.

4. Measuring Outcomes, Not Activity. Texas loves a summit and it loves a ribbon-cutting but let’s be fair, I can say the same of everywhere. Who doesn’t love a press release about a new innovation district? (Never mind the fact that press releases never reach anyone anymore). These aren’t outcomes. Outcomes are funding per capita in biosciences. Or number of biotech startups reaching $1M, $5M, and $10M in revenue. Look to new angel investors activated per year in life sciences or to exits and liquidity events. Measure local corporate procurement awarded to local biotech startups. If your bioscience ecosystem metrics look like event attendance and media impressions, you are measuring the wrong things, and your policy decisions will reflect that. This is explained extensively in why startup cities need to measure outcomes, not activity and in my book Startup Ecosystems.

5. Collaboration as Culture. Graham’s article celebrates collaboration at the state level for big institutional wins and Texas should be celebrated for that exceptional accomplishment. Collaboration at the startup level, where individual organizations share mentor pools, cross-refer founders, and integrate communications channels, that’s where the work gets hard and where most ecosystems fail. Stanford’s research on ecosystem performance shows that trust and informal collaboration networks are strong predictors of early-stage innovation output. Texas biosciences needs standing ecosystem roundtables that include startups, not just institutions.

6. Include the Invisible Talent. The OECD warns that untapped entrepreneurial potential disproportionately exists among people outside established networks. In Texas biosciences, this means the clinical researchers, the post-docs, the nurses and healthcare administrators with deep domain knowledge who have never been told they could be founders. What I saw in Phoenix, Arizona, is that they’re recognizing and fixing this. It means immigrant scientists on visas that make starting a company structurally difficult. It means the majority of people who never get invited to the summit in Austin (which reminds me, read about civic storytelling because a massive problem in most ecosystems is that no one even knows that such things are going on; please, everyone, learn how marketing works now and fix how you promote things). The stage cannot keep featuring the same handful of executives. More as to talent, use founder-assessment tools rather than resume filters. The best bioscience startups will come from people who don’t look like founders yet.

7. Architect Environments for Performance. Biotech startups need wet labs, BSL-2 facilities, prototyping resources, and access to clinical trial infrastructure. They need these things at startup-friendly price points, not at rates designed for Pfizer. The ACC Bioscience Incubator in Austin is doing this and TMC Innovation in Houston is doing this, but the gap between what exists and what’s needed is enormous, particularly outside of Houston. Workspace design, mentorship availability, early customers, and even psychological safety (biotech founding is isolating and grueling) determine whether founders move fast or stall.

8. Align Government, Academia, and the Private Sector. This is where Graham’s ARPA-H coalition model is genuinely instructive. The bow tie analogy I’ve used extensively applies perfectly here (applied a little differently): Texas invests heavily in on-ramps (programs, grants, accelerators) but often fails to tighten the knot where founders transition into revenue, customers, and capital. Universities produce research without commercialization pathways that actually work at speed. Government offers incentives but not deal flow. Investors wait for traction that can’t materialize without the infrastructure investors are waiting to see. Breaking this cycle requires shared KPIs across all partners and ecosystem stewards with actual authority to coordinate across institutions. Texas did this in ARPA-H and needs to do it for startups.

9. Accelerate Innovation by Unlocking Local Competitiveness. Texas biosciences has real comparative advantages.

- Houston owns clinical infrastructure and patient diversity

- Dallas owns diagnostics, medical devices, and now ARPA-H

- Austin owns the convergence of health tech and the “bio innovation tech stack,” as Scharf calls it

- San Antonio owns longevity science, military medicine, and infectious disease research

These are defensible regional strengths. If each city doubles down on its strengths rather than generically chasing “biotech” as a category, the state will develop the kind of focused ecosystem that outperforms generic ones. Saying “we do biotech” is like saying “we do tech.” It means nothing meaningful to the fact that people who work bio (or tech) don’t do the same things. Saying “we are the national leader in neurotech” (Austin’s case) or “we own cell and gene therapy manufacturing” (Dallas-Houston’s case) means everything.

10. Adapt, Don’t Copy. Texas should not try to be Phoenix or Boston, it’s not, I’m just stating it because it’s one of the 10 considerations and when ecosystems try to model what works elsewhere, they tend to fail. Do not try to replicate the Bay Area biotech model, which was built on decades of NIH proximity, Genentech’s founding mythology, and a real estate market that has since priced out most of the founders who would start the next generation of companies. Texas’ model should be built on Texas’ strengths: no state income tax, lower cost of living, massive patient populations for clinical trials, CPRIT’s non-dilutive funding model, the state’s economic development plan, and the cultural willingness to take risks that Graham described in his article. Adapt global best practices; don’t copy them. The regions that rise are not the ones that copy, but the ones that translate.

The Policy Gap That Nobody Wants to Talk About

Startups Are Not Small Businesses (here is a Texas Startup Policy Blueprint for Unlocking Capital) explored in Startup Economic Policy That Matters for Entrepreneurs, bears repeating here because biosciences magnify the problem. Texas does not formally distinguish startups from new businesses in its policy architecture. Fewer than roughly 10 to 15 percent of governments worldwide do this in law, policy, or administrative design. The Organisation for Economic Co-operation and Development has been explicit for more than a decade that high-growth, innovation-driven firms behave differently from small and medium enterprises and require different policy instruments, capital structures, and timelines.

In biotech, this distinction is even more critical because the timelines are longer, the capital requirements are higher, and the regulatory complexity means that a founder cannot “lean startup” their way through an FDA approval process. A biotech startup is not a small business with a microscope; it is an experimental venture operating under conditions of extreme uncertainty with capital needs that dwarf most startups by an order of magnitude. Treating it the same as a new restaurant opening in a Texas strip mall is not just unhelpful; it’s negligent. Texas’ overall policy trajectory is favorable (no state income tax, a business-friendly regulatory environment, growing research investment), but the lack of startup-specific policy instruments means the state is leaving enormous potential on the table.

Scharf noted in an interview with the Austin Monitor that policies like HB 1709, which sought to regulate business uses of artificial intelligence, could dampen enthusiasm for companies who see AI as critical to identifying health trends and creating new treatments. That’s the granular, sector-specific policy attention that bioscience startups need and rarely get. When your state legislature is debating AI regulation without understanding that 40 percent of your health tech startups depend on machine learning for their core product, we have a policy literacy problem.

Next for Texas Biosciences

Graham concluded the news of ARPA-H by saying, “The opportunity now is to make that the rule, not the exception.” He was talking about, I think, statewide alignment. I vehemently agree with his conclusion, and I’d extend it further: the ARPA-H coalition model worked because it had leadership, specificity, shared goals, and accountability. Apply that same model to the startup ecosystem itself and Texas biosciences goes from being a state with great institutions that happens to have some startups, to being a state where great institutions exist because the startup pipeline feeds them.

Concretely, that means establishing a bioscience-specific startup development organization (or empowering an existing one) with a mandate to coordinate across all four major cities. It means CPRIT explicitly partnering with startup accelerators and incubators to create warm handoffs from grant recipients to founder development programs. It means building a functioning bow tie where the knot connects university research, regulatory strategy support, clinical trial access, and early-stage capital into a single navigable pathway for founders. It means treating ecosystem builders like infrastructure, not volunteers. It means measuring whether startups are actually surviving, growing, and generating returns; not whether an annual summit had good attendance.

Thomas Graham wrote that “the future of biosciences in Texas is not just promising. It is already here.” The 2025 data says he’s righter than even he may have anticipated. Garheng Kong, Founder and Managing Partner of HealthQuest Capital, captured it well in the 2025 Report: “Austin brings together a rare mix of strengths that make healthcare innovation possible at scale. You have leading technology talent, a growing device, diagnostics, life sciences ecosystem, forward-looking health systems, and access to capital, all in one market. What excites me most is the entrepreneurial mindset here.” And Claudia Lucchinetti, Dean of Dell Medical School, framed the broader ambition: “What’s happening in Austin isn’t just the growth of individual companies. It’s the creation of a new model for how a region advances human health. We’re aligning research, clinical care, education, and innovation in ways that rarely happen in the same place at the same time.”

On the institutional side, Texas is demonstrably a national leader; on the startup side, the trajectory just crossed its own inflection point. A $77 billion ecosystem that grew 45 percent in a single year is not a state still figuring things out; it is a state where the flywheel is turning and the question has shifted from “will this work?” to “how do we make sure the infrastructure keeps pace with the momentum?” The materials are not just on-site; they are being assembled at speed. The blueprint is being drawn by people who actually understand what they’re building. Whether it becomes the definitive model for bioscience entrepreneurship outside the coasts depends on whether the ecosystem builders, the policymakers, and the capital allocators treat this moment with the seriousness it deserves. But for the first time, the data says the bet is working.

If you’re a founder in Texas biosciences trying to figure out why the ecosystem simultaneously looks amazing on paper and feels like it could serve you better in practice, you’re paying attention, and you’re right to expect more, because more is coming. You’re paying attention and I want to celebrate you for that, encourage you get more involved, comment, and raise your expectations even higher. If you’re an investor wondering why the deal flow doesn’t yet fully match the institutional momentum, the answer tends to be, and is here, in the infrastructure between the lab and the cap table. And if you’re an economic development professional reading this and nodding, stop nodding: let’s start filling in the gaps. The playbook exists.

The Bio & Health Ecosystem in Austin is booming and the Texas Triangle is speeding up. When we lean into unique strengths of each region, it is going to be something truly special.

We are still so early

Jason Scharf I keep chewing on how we need to rethink that triangle by sector… in energy, it extends from Houston to Midland. You’re exactly right, unique strengths that accelerate in concert.

Paul O’Brien, I am a strong believer that Texas will be stand together as a community.

Yesterday at hashtag#BiofestInvest, I watched founders, clinicians, and investors sit in the same room — not as competitors, but as builders. That’s the Texas I know. That’s the Texas I’m building for.

And we’re just getting started.

Health House is coming to SXSW 2027 — a multi-day activation in Austin bringing global HealthTech minds to the heart of where community actually happens.

One conversation. One connection. One story that changes everything.

Stay close. ?

Paul O’Brien fair. It is really just TEXAS

That’s incredible!

Curative

Think what the corridors would look like if those were independent rail tracks truly connecting, sustainably and efficiently, the eco-systems! 🙂

Mary Shepard Spaeth Economic Development Zones are severely underutilized or developed. We must stop organizing ecosystems around city borders and identities.

Bingo! Paul O’Brien Spot on – both on the massive opportunity and the structural holes. Working on the digital infrastructure to interconnect disconnected communities to unleash the hidden value. Kudos to all the unsung heroes like you and so many others who are building ecosystems with limited resources!

Paul O’Brien by region, by sector, by stages, by tech, by market… multidimensional segmentation needed. Fun exercise for the day.

Great summary Paul! And 2026 seems to be starting off strong as well, especially with the recently announced $300M deal for Eli Lilly and Company to acquire CrossBridge Bio.

Big Bayer ‘s CEO since 2023 is a hashtag#ChemE from @school/theuniversityoftexasataustin-, then Massachusetts Institute of Technology – Bill Anderson @servinglifescience

The Texas Triangle is the future, in my opinion, of global economic influence if we continue to be thoughtful with our investments and planning – finance, energy, sciences – all accounted for and booming.

Thomas Graham, I’d add “computing” to that list, intentionally using that term; not “tech” generically.

Samsung and Texas Instruments in semiconductor fabrication, data center infrastructure growing faster than the grid can keep up with, quantum computing research emerging from UT Austin and Texas A&M. When you stack energy to power compute, financial infrastructure to capitalize it, and biosciences to apply it, there’s a sector foundation.

What I tried to map in this piece is whether the startup layer underneath all of that institutional momentum is keeping pace. Your CHART coalition proved four cities can align around shared outcomes when someone architects it deliberately.

That same model applied to the startup pipeline and Texas needs to do more of it with the same sophistication Texas’s strengths in the other sectors.

What was your data source for the ‘extensive audit’? The balance of the $2.07B feels small, given what’s happening at Pegasus Park.

David, dozens… This isn’t a peer-reviewed forum and there is no reason to cite everything I went through to come to what’s here, my articles are long as it is.

No doubt it’s incomplete, it’s an article, not funded research.

Is anything I covered incorrect?

What’s missing?

Paul, I enjoyed this article and have a few things I am curious about.

Your section on environments for performance hits on a hot button I see for clients. The high end lab space that has been built is way too expensive for the companies that are here and the local players seem to disagree. I’m not sure how else to explain to them that my clients in other markets are getting better deals on their lab space by orders of magnitude than they are here locally. The more expensive markets like Boston and San Diego have so many other advantages we won’t win the battle of being slightly cheaper on real estate costs.

Also, regarding Houston, you talk about clinical infrastructure. Are you lumping advanced manufacturing infrastructure like CDMOs into that? Houston has a growing and strong cGMP ecosystem that I don’t think is getting enough attention. There are so many different advanced drugs being developed and trialed but the conversation often doesn’t seem to include actually manufacturing them. The ability to do that only further helps biotech startups.

Zachary Leger “the local players seem to disagree” is one of the reasons I can be such a pain in the ass about distinguishing things properly… of course the capably funded companies, City, sponsors, and property owners, will say whatever is necessary to look good and promote what they’ve done.

For “Startups,” you’re absolutely right and that’s my point. Our approach to physical space, and funding for it, is horrific in Texas as it pertains to truly serving the entrepreneurs.

Detractors can keep disagreeing with me (and you), but they’re either lying, ignorant, or don’t care (one of those things must be true)

I get in a similar battle with University Tech Transfer Offices who hate that I point out that they’re broken. Sure… the model works “for them” but only about 2% of University Research gets commercialized so they can all shut it when we point out that it what they’re doing isn’t working.

As for Houston…. you’re taking it to the more sophisticated degree than my work or the goal of this piece. I push things forward broadly so as to fix the gaps… my specialty is startup ecosystems and the respective economic development. When we go deeper on any sector, I have to call the experts.

Amusing that “Biosciences” never includes Agricultural Biotechnology. As an old colleague used to say – “If you don’t feed the poor bastards, they starve to death before living long enough to develop diseases that require expensive pharmaceuticals”. Sector growth only projected to $140–$245 billion. Maybe follow the example of the Danforth Center in St. Louis.

Alan Gould Its there, its just not as sexy. Saying you can increase bushels an acre, is not like curing cancer, in investors minds. There is bio in ag, only it has gotten off to a rough start. Too many startups with high valuations and little return. Bio in ag should be more than “bugs in a jug”, like is the case in most other bio heavy industries. Again, it is sexier saying you are in the biological space versus found a way to make better inputs.

Alan Gould that’s fair. We didn’t include it in the report as we were limiting it to human health, so no vet or ag. Partially driven by neither Jani Tuomi or I having much experience in the space (Ag was a small business line at illumina, when I was there)

At the same time there is overlapping fundamental tech and you make a great point on the importance of the food stack.

Jason Scharf some of the research in AG Tech is absolutely fascinating and something I am keen to learn more about.

As I mentioned before – check out The Danforth Center in St. Louis. A powerhouse in plant genetics and biotech.

Alan Gould The Danforth Center was established with significant support from Monsanto Company , now Bayer | Crop Science .

Paul, the institutional wins are real and earned — but you’ve identified the harder question: does the startup layer keep pace with the infrastructure being built around it?

We’re seeing this firsthand with investments across Houston, San Antonio, and Dallas. The regional density you describe isn’t just a policy thesis, it’s the operating reality we’re building into. And the distinction you draw between the Valley of Death and the structural missing middle matters more than most ecosystem discussions acknowledge.

San Antonio anchoring ARPA-H longevity science through the Barshop Institute makes this particularly concrete for us. The infrastructure for turning breakthroughs into market-ready solutions is being assembled and the venture ecosystem now has to keep pace with it.

The full stack or nothing. Great analysis.

Love seeing this and excited to see more development cross Texas especially in Houston!

Check it out, Robert LaGesse

The jump from 18th to 6th in health VC in a single year is the headline number, but the durable signal is the coalition layer behind ARPA-H landing at Pegasus Park. Capital flows follow infrastructure flows with a 2-3 year lag — institutional anchors (ARPA-H, TIBIR, UT Southwestern) de-risk the next vintage of founders. Worth watching whether Austin can convert this into a translational medicine cluster or whether it stays dominated by health-tech software plays.

Capital flows follow infrastructure” Exactly why I wrote a book to explain Ben Carroll

Too many cities are still calling to share that their ecosystem is focused on capital… while lacking the infrastructure or economy that makes it valid.