Today at the Texas Venture Forum in Austin, TX, we had the honor of hearing from the 28th Administrator of the U.S. Small Business Administration, Kelly Loeffler. Loeffler, a former business executive, co-owner of a WNBA team, and founder of a commodity exchange, now carries a unique blend of corporate, public, and policy experience to the SBA. Her presence in Austin wasn’t just symbolic; it was substantive. She came with clarity, candor, and conviction — and it’s about time.

Loeffler spoke at length about what she calls “New Collar Jobs,” a phrase that might sound like a rebranding exercise at first, but it’s anything but. In remarks echoed from past addresses, including during her time with Intercontinental Exchange and in her Senate speeches, Loeffler defined New Collar Jobs as the work of America’s skilled labor force — not necessarily armed with college degrees, but equipped with certifications, trade skills, and practical expertise. These are the jobs building our EV infrastructure, running logistics, maintaining AI-powered robotics, managing precision agriculture, and restoring America’s competitiveness in manufacturing. They are, in a word, essential.

What makes her framing powerful is that she ties it to a broader economic and political vision, under her leadership, unapologetically practical:

- Increase access to capital

- Reduce regulation

- Incentivize trade schools

“Get the government out of the way so people can innovate, hire, and invest,” she told the room, met with applause. Because here’s the truth: Trade schools are not the fallback plan for students who can’t “cut it” at university. They’re exceptional, focused alternatives, often leading directly to high-paying, high-demand careers. And with the student debt crisis still casting a long shadow, it’s time we celebrated those who pursue certifications over diplomas.

When pressed on why this triad of policy focus matters now, she added, “It can feel like we’re a country that worries about ‘what if’ instead of ‘what can be.’ Do more, reach higher, and celebrate success.”

The SBA has made significant inroads toward these goals. Between SBIR (Small Business Innovation Research) grants and the longstanding SBIC (Small Business Investment Company) program, the agency has tools to support everything from R&D to capital formation. Their new push in 2025 emphasizes regional engagement, streamlined applications, and partnerships with local lenders and ecosystem builders. But as Loeffler herself acknowledged, “We need people more like all of you, innovating and pushing Washington.”

That brings me to the real purpose of this article.

Increasingly Clear: Distinguish Between Startups and Small Businesses

I’ve spoken on this before. Occasionally written about it. But the conversation today — paired with recent developments in Europe — makes it all too clear: We’re at a turning point.

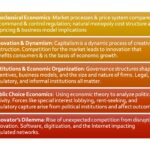

The European Union is in the process of relaxing restrictions on private equity, specifically to foster a more robust venture capital environment. Their reasoning? I’m sure it wasn’t because I told them to, but it is to better emulate the U.S. startup ecosystem. What that implies, and what every serious government and policy strategist must recognize, is that there’s a fundamental difference between launching a startup and opening a business.

A startup is a temporary endeavor, designed to search for a scalable, repeatable business model. It is inherently uncertain. It often exists in stealth, loses money for years, pivots rapidly, and scales globally, if it survives at all. A small business, by contrast, is launched to operate. It’s a deli. A CPA firm. A local IT services company. Equally important, yes, but fundamentally different in purpose and policy need.

When Loeffler says, “We need people more like all of you,” she’s talking to the venture capitalists, the scrappy founders, the innovators who operate on hope, not spreadsheets. She’s recognizing, I think, that the startup economy isn’t just a wing of the small business world, it’s a different animal entirely. And if we want to support it, we need different cages, tools, and caretakers.

New Collar Workers who innovate, inspire, engineer, and create both the wealth and jobs that drive economies.

Startup White Paper

That’s why I’ve been so vocal about this issue. Because the more we confuse the two, the more we fail both. Investors misallocate. Universities miseducate. Governments misfire. And founders? They pay the price.

Which is why, today, I’m releasing a white paper titled: “Why Governments Must Distinguish Startups from Small Businesses.”

This startup white paper outlines the policy rationale, economic research, and operational differences between these two types of ventures. It provides a framework for how we might establish a distinct Office of Startups and Innovation within the SBA — one that treats innovation as a public good as it is starting to do, not just a buzzword.

The paper can be downloaded with an email address, and I invite policymakers, ecosystem leaders, and founders alike to give it a read. We can’t afford to build tomorrow’s economy with yesterday’s assumptions. The line is drawn. It’s time to act accordingly.

Related articles:

Startup Ecosystems Fail Because of Investors

Startup Ecosystems Fail Because of Investors

How the 2025 White House Could Shape a Bold Economy for Startups and Innovators

How the 2025 White House Could Shape a Bold Economy for Startups and Innovators

The Startup Scorecard: How Governments Can Unlock Trillions in Innovation and Economic Growth

The Startup Scorecard: How Governments Can Unlock Trillions in Innovation and Economic Growth

10 Policies Proven to Turn Cities into Startup Powerhouses

10 Policies Proven to Turn Cities into Startup Powerhouses

What Startups Can Learn from Utility Regulation: How Northwestern’s Five Prisms Reveal the Blueprint for Disruption

What Startups Can Learn from Utility Regulation: How Northwestern’s Five Prisms Reveal the Blueprint for Disruption

Such a fire article – its why I took US pre-seed and so wish I had an ecosystem like Cup of Joey the UK only has a small business mindset and thats a big struggle for me, the ecosystems I have – nothing offers me something similar to the US startup ecosystem and why I take part in some of Fusion42 workshops – they are

Im not a SME, Im messy and thats a startup.

Georgina Bowman Absolutely love this—couldn’t have said it better myself. That line “I’m not a SME, I’m messy and that’s a startup” needs to be framed on every accelerator wall from Manchester to Miami. The UK’s focus on SMEs is powerful for stability, but when you’re building something that doesn’t exist yet—something scalable, chaotic, high-risk, and transformational—you need a different kind of ecosystem entirely. That’s why distinguishing startups from small businesses isn’t just semantics, it’s survival. Let’s keep building bridges across the Atlantic so more founders like you get what they actually need.

Paul O’Brien support and understanding is what I need and Innovate UK are getting their with me, watch my post tomorrow! BUT!!! – this help should have come way sooooner.

Georgina Bowman , we will be glad to support Cup of JoeY “across the pond”

This is great, Paul O’Brien. Will definitely give it a read. Great to meet you at the gala tonight. Let’s meet for coffee some time and compare notes!

We need to stop confusing startups with small businesses.

“Why Governments Must Distinguish Startups from Small Businesses”

This isn’t just theory — it’s a framework for federal policy.

? How the SBA could create an Office of Startups and Innovation.

This distinction between new-collar jobs and traditional roles is pivotal for our evolving economy, Paul! As we embrace this shift, it’s essential to recognize the potential of microbusinesses as a vital classification within this landscape.

Microbusinesses embody the spirit of innovation and resilience, often led by passionate individuals who bring unique solutions to the table. By advocating for their recognition, we empower these entrepreneurs to thrive, fostering a culture of autonomy and leadership that can drive our communities forward.

Bring back welding!!!! (UAV Orchestration Manager III more likely), looking forward to reading the white paper and great seeing you yesterday.

Love this!

Less regulation? Hell no. Better regulation? More appropriate regulation? More efficient regulation? Absolutely. When scammers and cheaters can get away with scamming and cheating, it fouls the entire system.

Education in the trades? Absolutely! More paths are good. But you also have be careful of creating a disposable class of workers whose skills can be perishable. That’s just a lot of the history.

If you want a healthier startup ecosystem, look toward fixing housing and transportation and medical care; failure has to be easier to get past to broaden the talent pool beyond those with means. There will be down times.

I’ve been thinking about this (i.e., your distinct – and spot-on – definition of startups) as well as your recent context of investors. I have an analogy that might help.

Startups are like the early – circa late 1400s and forward – explorers. They had investors but those investors were all but certain they weren’t going to see a return on their investment. Heck, they were mostly certain they’d never see the investee again. lol

If there’s a must-see pitch deck, it’s Chris Columbus’.

Or Magellan? Around the world? Man, what was he smoking? Who would invest in that? What were they smoking?

And the rest is history.

If you’re thinking “This is crazy” a/o “This is going to be money I’ll likely never see again” then chances are 99.99% it’s a startup (or a grifter). Else it’s a (small) business.

Great points, again. I’m looking forward to checking out the whitepaper.

For too long start-up culture has been defined by VCs – for their own benefit. It’s overdue to give that power to the founders themselves. They are the ones defining a new world, not financiers.

“No collar” would better describe startups.

Hello black t-shirt!